One of the more dangerous things happening in venture right now is not simply that AI is attracting absurd amounts of money. It is that AI is making the entire market look warmer than it really is. That distinction matters because founders do not fundraise inside headlines. They fundraise inside actual market conditions. And right now, the headline market and the lived market are diverging in a way that is producing a lot of bad founder behavior: inflated pricing expectations, confused process design, bad benchmark comparisons, and a persistent feeling that “everyone else is getting funded except us.” In many cases, everyone else is not getting funded. You are just looking at a blended number that hides the split.

The cleanest way to say it is this: AI has not merely become a large sector inside venture. It has partially broken the usefulness of aggregate venture statistics.

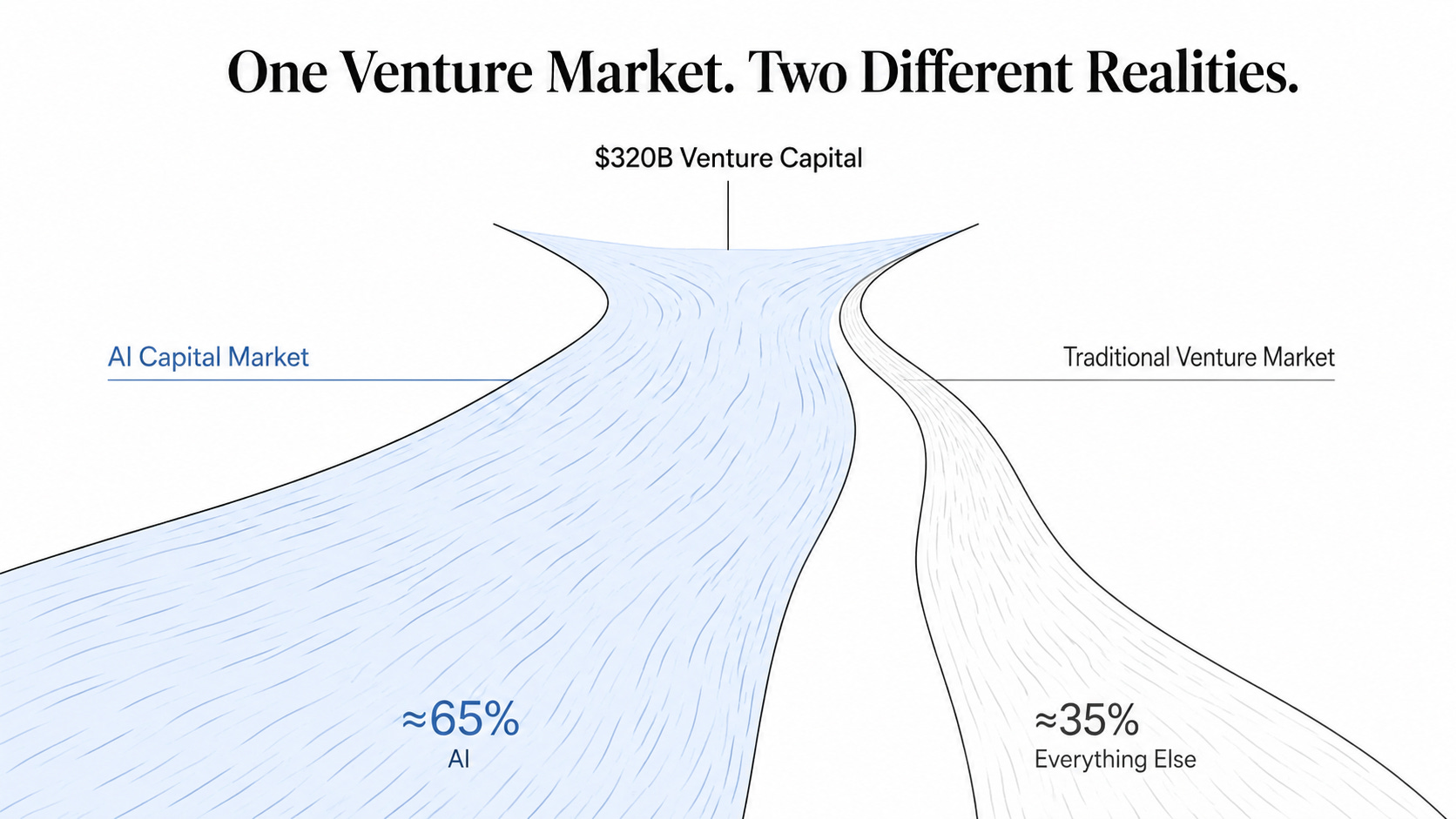

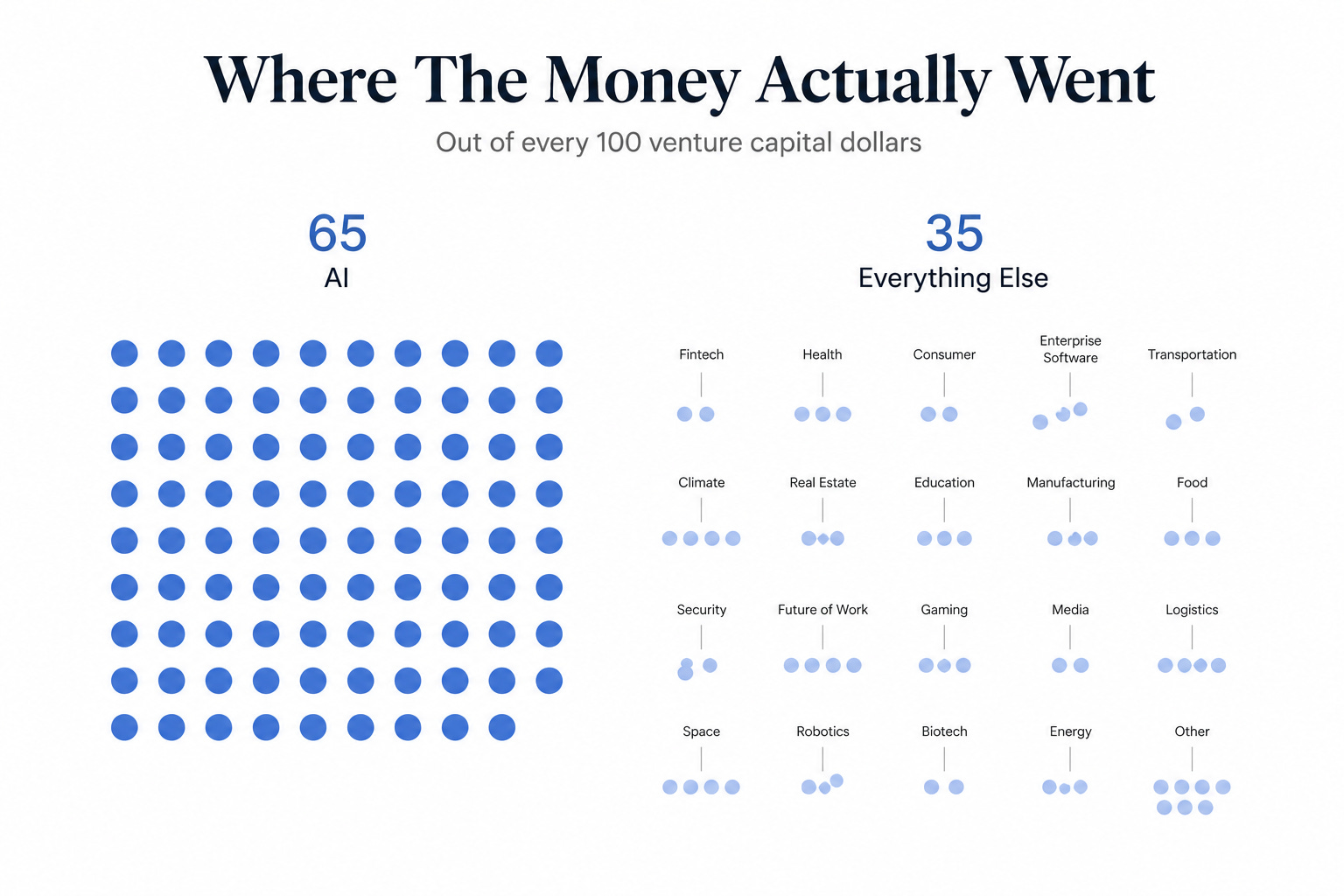

The NVCA’s 2026 Yearbook basically says this out loud. US venture deployed $320 billion across 15,352 deals in 2025, but the report says the headline number describes “two markets stacked on top of each other.” AI accounted for 65.4% of total deal value. The top five companies alone raised nearly $60 billion collectively. Strip out the mega-round layer and the rest of the market looks much more ordinary. NVCA puts it bluntly: remove the mega-deals and the remaining roughly 14,865 deals totaled about $105 billion, a solid but unremarkable market that looked a lot more like 2019 or early 2020 than like some broad venture boom.

That is not a minor accounting adjustment. That is a completely different founder reality.

It means a huge number of founders are reading “venture is back” and hearing “capital is loose again,” when the more accurate message is: capital is very loose for a narrow class of AI-linked companies and much more disciplined for everybody else.

Q1 2026 only made the distortion more extreme. PitchBook and NVCA reported $267.2 billion in quarterly deal value and $347.3 billion in exit value, both record-looking figures. But if you exclude the five largest deals and exits, those totals fall by 73.2% and 86.6%, respectively. That is not normal skew. That is concentration so extreme that the top line becomes almost theatrical. And the concentration is not just at the very top. The same Q1 2026 report says 88.8% of Q1 deal value went to AI. AI accounted for 42.5% of deal count, more than half of megadeals, and more than half of CVC deals. AI companies that closed rounds in Q1 did so roughly half a year sooner than non-AI companies. The report also shows AI valuations sitting materially above non-AI valuations across stages, with AI companies moving through the early venture lifecycle faster and with higher step-ups.

That is not “a hot sector.” That is a parallel market with different physics.

And once you understand that, a lot of the confusion founders feel right now starts to make more sense.

I keep seeing founders benchmark themselves against the wrong part of the tape. They read about giant rounds, compressed timelines, aggressive pricing, pre-emptive behavior, and frantic investor urgency, then assume that is the ambient market. It is not. It is the ambient market for a subset of companies that sit close to the current AI capital flywheel: model labs, infrastructure, chips, compute, tooling, strategic enterprise wrappers, and a smaller set of application companies that have either real escape velocity or unusually strong strategic positioning.

Everyone else is still fundraising in a much colder emotional climate. That does not mean dead. It does not mean impossible. It does mean slower, more selective, more proof-sensitive, and far less forgiving of ambiguity. That difference sounds obvious when you say it plainly. But founders behave as if it is not true all the time. They push for prices that were implied by someone else’s market. They expect speed that belongs to someone else’s market. They assume investor hesitation is irrational because the news says capital is flooding back. They run broad outbound processes when what they really need is narrower investor-fit and tighter milestone logic. And they start blaming storytelling when the real problem is that they are pitching a normal company into a distorted benchmark environment.

This is why I think “AI has split venture into two markets” is more useful than the simpler line that “AI is eating venture.” The latter is true, but it is not operationally useful enough for founders. The former is. It tells you that your fundraising strategy should begin with a more honest question:

Which market am I actually in?

If you are in the hot AI market, the game is often about allocation, speed, narrative control, strategic signaling, and how quickly you can convert enthusiasm into price without losing the round’s long-term quality.

If you are in the colder market underneath, the game is very different. It is about proof density, precise investor fit, clean milestone design, and making the case feel underwriteable enough that somebody will actually want to carry it internally.

Those are not cosmetic differences. They should change the entire process.

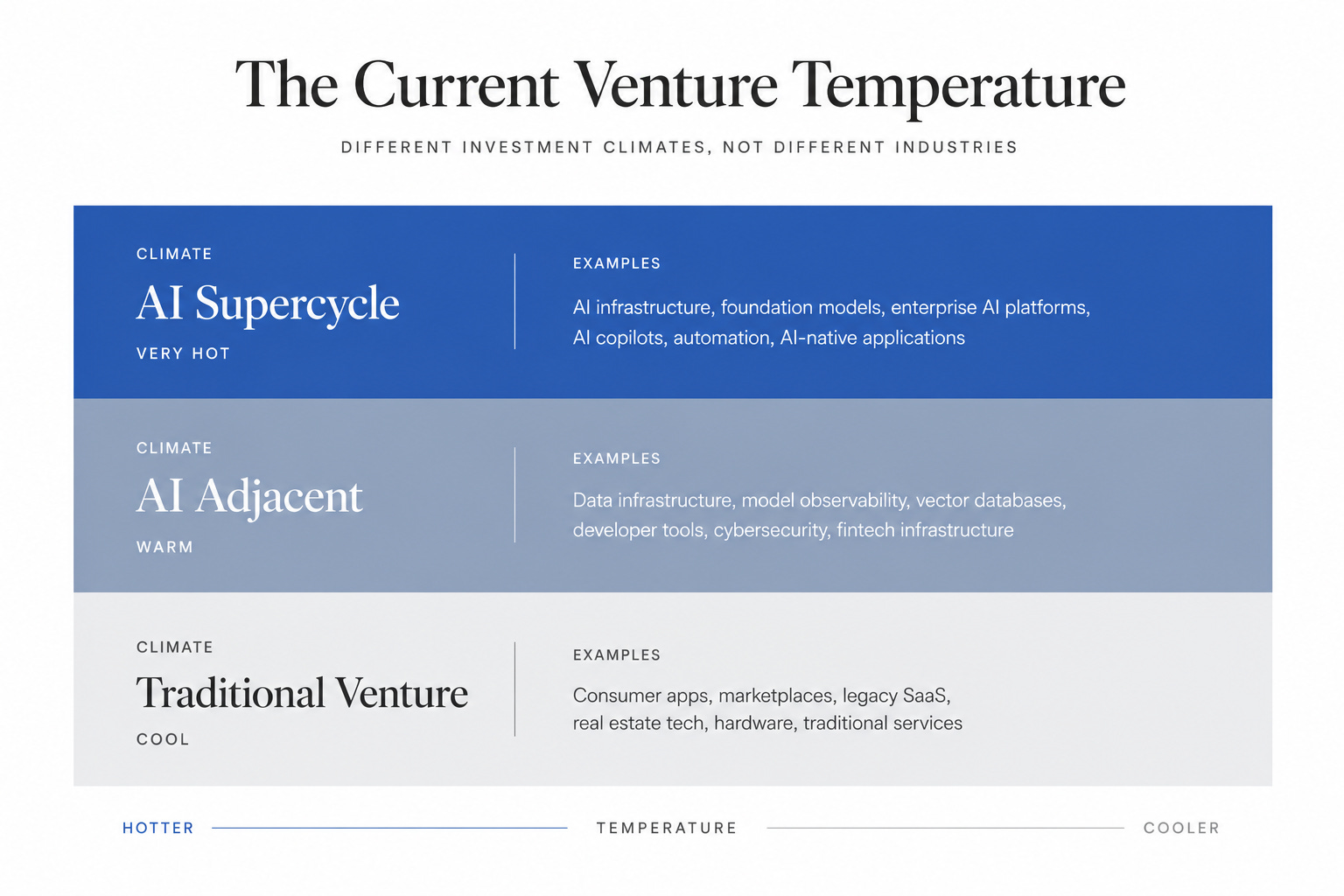

Even more importantly, founders should understand that the split is not simply “AI versus non-AI.” That would still be too crude. There are really at least three buckets hiding inside the current market.

The first bucket is the obvious one: companies sitting directly inside the AI supercycle. These are the businesses close enough to infrastructure scarcity, model leverage, distribution advantage, or strategic compute relationships that capital is behaving competitively around them.

The second bucket is the “AI-adjacent but not truly exempt” category. This includes many application-layer companies that use AI in a real way but do not command the same strategic urgency. Some of them benefit from the halo. Many do not. They discover, usually painfully, that saying “AI” in the deck does not actually move them into the hot market unless the rest of the case supports it.

The third bucket is everything else: good software, vertical SaaS, fintech, healthtech, climate, industrial, services-enabled models, marketplace variants, and a long tail of serious companies still being priced by more traditional venture discipline.

That third bucket is where a lot of founders get hurt right now, because they are still running a 2021-style or AI-headline-shaped process inside a market that wants 2019-style clarity.

That mismatch shows up in a few predictable ways.

First, founders overprice the round. They see the gross numbers and assume investors are broadly flush, loose, and willing to move. In reality, the money may be concentrated into very few firms and very few companies. PitchBook and NVCA report that 73.1% of the capital committed in Q1 2026 went to five VC firms. NVCA’s Yearbook says 2025 fundraising fell to $67 billion, the lowest level in nine years, and just 101 first-time funds closed, the lowest count since 2007. The Q1 2026 summary page adds another uncomfortable detail: for most investors, single-digit IRRs and sub-1x distributions are still the norm. That means the supply of patient risk capital for most normal deals is not expanding in some uniform way. It is concentrating while much of the rest of the asset class is still waiting for real liquidity.

Second, founders misread speed. If AI companies are moving roughly half a year faster between rounds than non-AI companies, then using AI deal cadence as your benchmark is a good way to decide you are failing when you are simply in another market. That psychological error matters. It makes founders panic, widen the process, accept bad-fit capital, or start revising the story every ten days because they think the issue is communication rather than market lane.

Third, founders start performing AI. I do not mean they all pretend to be model labs. I mean they reshape the pitch around whatever seems to trigger current investor appetite, even when the real company is being built on a different logic. This usually creates uglier problems later. If the round clears because the company borrowed the valuation language of the hot market without earning its underwriting logic, the next round tends to be nastier, not easier.

You can already see symptoms of that distortion in the market. The Wall Street Journal reported earlier this year that some AI startups have used dual-tier fundraising structures to create the appearance of sharper valuation acceleration, with different investors entering at different prices only days apart. That is not the behavior of a calm market discovering price cleanly. That is the behavior of a market where heat itself has become part of the product.

Founders outside that loop should not envy it too casually.

Hot markets create their own traps. They can subsidize bad discipline, inflate option strike issues, distort hiring expectations, and pull mediocre companies forward on terms that later become difficult to defend. But the more immediate problem for most founders is not that the hot market exists. It is that they keep pretending they are in it.

That is where strategy starts to go wrong. If you are not in the hot lane, stop building the process around hot-lane assumptions. Raise the amount the colder market can actually underwrite. Set milestones that change the financing answer rather than just making the story busier. Target investors whose thesis genuinely matches the company instead of trying to manufacture a generalized feeding frenzy. Expect more diligence, more valuation sensitivity, and less tolerance for conceptual hand-waving. And above all, stop reading mega-round headlines as evidence that your own market has become easy again.

This is one of those moments where founder psychology and fund mechanics are colliding in a particularly unhelpful way. Headlines tell founders the market is roaring back. Their own processes tell them investors are selective, slow, and still asking unromantic questions. Instead of trusting the lived signal, many founders assume they must be doing something wrong.

Sometimes they are. But often they are simply standing in the wrong market and borrowing expectations from another one.

I think senior investors already understand this split intuitively. They know the aggregate numbers are hiding multiple realities. They know a small set of AI companies is absorbing not just capital but also urgency, attention, and tolerance for imperfection. They also know that outside that lane, the old disciplines still matter: wedge, distribution, proof, retention, market shape, pricing power, ownership logic, and whether the company can survive scrutiny without a huge macro narrative doing the heavy lifting.

Founders need to internalize the same thing.

The next twelve months are not likely to become less bifurcated. If anything, they may become more so. The Q1 2026 report suggests OpenAI and Anthropic IPOs could become transformational liquidity events if they land well. If they do, the AI loop may get even more intense. That will create more headlines, more envy, and more confusion for founders building outside the center of the current trade.

The right response is not resentment. It is segmentation. Understand which market is actually setting your terms.

Because if you misdiagnose that at the start, almost everything downstream gets worse: the pricing, the timing, the outreach list, the story, the milestones, the emotional read on investor behavior, and eventually the quality of the cap table itself.

Most founders do not need a better opinion about AI. They need a better opinion about which venture market is actually theirs.