Mountain wears her distinctive blanket with city below .

Menu of the day

Markets: chips outrun inflation

The article: money gets an API

Shot: credit, hardware, and builder tokens

Startup Lesson: model the boring bits

Doggy Bag: T-bills with Wi-Fi

What to watch: rails and rates

Market pulse

The market is doing that charming thing where it reads hot inflation data, nods seriously, then buys chips anyway. U.S. equities pushed to fresh records on Wednesday, with the S&P 500 up about 0.6% and the Nasdaq up about 1.2%, helped by another rebound in AI-linked semiconductors. The Dow slipped, which is useful mostly as proof that not every ticker was invited to the party.

Asia kept the mood alive on Thursday, with AI enthusiasm strong enough that investors could briefly pretend oil above $100, higher-for-longer rates, and a Trump-Xi summit were just decorative background objects. SK Hynix has become the kind of stock chart that makes rational people whisper, “Maybe just one more leg.” That usually means the story is powerful, crowded, or both.

For founders, the message is still fairly simple: capital likes growth, but it loves growth attached to infrastructure, payments, compute, compliance, or real operating budgets. The market is not rewarding imagination alone. It is rewarding imagination with a socket, a contract, or a line item.

The article: The wallet joins the workflow

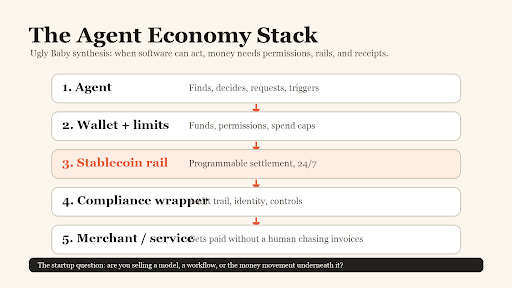

The funny thing about AI agents is that everyone wants them to do work, but very few people want to talk about how they get paid, what they are allowed to spend, and who signs the receipt when the tiny robot goes shopping. We have spent months discussing agents as workers. The next conversation is about agents as economic actors, which sounds futuristic until you remember that most business software eventually becomes a payment problem wearing a nicer interface.

Circle just gave that conversation a useful shove. The company reported $694 million in first-quarter revenue and reserve income, up 20% year over year, with USDC circulation at $77 billion and on-chain transaction volume at $21.5 trillion. At the same time, it disclosed a $222 million presale for ARC tokens tied to Arc, its enterprise blockchain network. It launched Agent Stack, a set of tools meant to let AI agents hold funds, discover services, and make programmable payments with guardrails.

The headline version is easy: stablecoin company does stablecoin things. The more useful version is that Circle is trying to move from being the “issuer of a dollar token” to being the “operating layer for internet money.” That matters because reserve income is a nice business when rates are friendly, but it is not a forever moat. If rates fall, if banks issue competing tokens, or if regulation changes the economics of stablecoin rewards, Circle needs to own more than the coin. It needs to own the activity around the coin.

In practice, Arc and Agent Stack are an attempt to sit beneath a future in which software not only recommends actions but also executes them. An agent books a supplier. An agent pays for a dataset. An agent buys compute for a task. An agent settles a small service fee after completing a workflow. Traditional banking rails can do many things, but they were not designed for tiny, frequent, programmable transactions between software objects that need permissions, limits, identity, and audit trails.

This is where stablecoins become less crypto-theatre and more financial middleware. The boring pitch is not “number go up.” The boring pitch is “this payment can move at 2:13 a.m., across borders, under a spend limit, with a record attached, without asking three institutions to wake up.” Boring, in finance, is often where the money hides. The suit is ugly, but the pockets are deep.

There is also a regulatory wrinkle. The U.S. crypto market structure debate is still moving through the usual democratic spa treatment: markups, compromises, lobbyists, and everyone pretending the one clause they like is civilisation itself. Stablecoin rewards, developer protections, and who gets to do what under which regulator still matter. But Circle’s move is interesting because it is not waiting for one perfect outcome. It is building a layer that can be useful whether the stablecoin business becomes more open, more bank-like, or more tightly supervised.

That is a founder lesson hiding inside a public-company move. The best infrastructure businesses do not depend on a single legal model. They work across plausible futures. If the world loves stablecoins, they benefit. If institutions want tokenized funds, they benefit. If AI agents need programmable payments, they benefit. If regulation forces more compliance into the stack, they can sell the guardrails. That is much better than building a startup whose business model requires Congress to behave elegantly. Historically, not the safest KPI.

The startup implication is broader than crypto. Every agentic workflow eventually touches trust. Who can spend? How much? On what? Under whose identity? With what approval path? What happens if the agent buys the wrong thing, pays the wrong vendor, or gets tricked by a very persuasive PDF? The companies that solve those questions may not look as exciting as the model labs, but they may become the systems that make agentic software usable inside real companies.

This is the same pattern we keep seeing elsewhere. AI products are becoming less about impressive output and more about operational permission. Yesterday, the question was whether an agent could call a customer, update a CRM, or process a document. Tomorrow, the question is whether it can transact safely. Once money enters the workflow, the product stops being a demo and starts being infrastructure with lawyers attached.

For early-stage founders, the takeaway is not “build a stablecoin startup immediately, preferably by Monday.” Please, breathe. The takeaway is to look at the workflow you are automating and ask where value actually moves. Is the bottleneck a decision, a payment, an approval, a reconciliation, a compliance step, or a trust problem? If the workflow ends with someone manually copying data into another tool, chasing an invoice, or asking finance for permission, the automation is not finished. It is just wearing nice shoes.

The next wave of useful AI may therefore be less magical and more transactional. Models will act. Wallets will constrain them. Payments will settle. Audit trails will explain what happened after everyone has already panicked. And somewhere in that stack, a few companies will make a lot of money by making the whole thing boring enough for enterprises to buy.

Bottom line: the agent economy does not only need brains. It needs rails, limits, receipts, and someone responsible when the software decides it has excellent taste in vendors.

The hard part is not giving agents money. It is giving them limits, context, and a receipt trail.

Shot: Credit wakes up with a calculator

If rates start drifting lower over the next cycle, lending technology gets interesting again. Loan origination is brutally cyclical: when rates are high, volume falls; when rates ease, every lender suddenly remembers growth exists and starts looking for better tooling. The obvious AI pitch is “better underwriting,” but that may be too lazy. Underwriting has used models for decades. The fresher opportunity is around the messy edges: collecting borrower data, guiding applicants, servicing loans, detecting fraud, and communicating with customers across the life of the loan.

The founder read is simple: do not sell magic credit intelligence if the buyer already trusts their underwriting model. Sell lower friction, better conversion, cleaner servicing, and fraud defense. In lending, boring workflow improvement can be worth more than pretending the model discovered repayment risk last Tuesday.

Shot: Hardware is back in the room

AI keeps making software people rediscover objects. Data centers are not made of vibes. They are made of power systems, cooling, servers, networking gear, storage, land, permits, cables, and enough electrical work to humble anyone who thinks infrastructure is a Figma file. This is why some of the more interesting AI winners are not model wrappers but companies selling the physical and operational picks-and-shovels around the boom.

For startups, the lesson is slightly uncomfortable: the closer your software sits to a hard operational bottleneck, the more defensible it may become. Hardware-enabled software is annoying because deployment is real. That is also the point. Reality is a moat when everyone else is shipping a dashboard.

Shot: Developer credits are distribution now

Claude is giving paid users a monthly Agent SDK credit from June 15. Small detail, useful signal. The frontier labs are not only competing on model quality anymore. They are competing to make developers build habits, workflows, and small internal machines on top of their tooling. Free or included credits are not charity; they are a polite way to turn experimentation into usage.

This matters for AI startups because the distribution battle is moving into the build environment. If your product depends on developers, you are not only competing with other startups. You are competing with the default rails, credits, templates, and SDKs that bigger platforms slide into the path before you even arrive.

Startup Lesson: Model the boring bits

A financial model is not a fundraising ornament. It is the place where the investor checks whether the founder understands the business without the pitch voice turned on.

The weak model is easy to spot: one growth curve, one salaries line, one beautiful margin expansion that appears by spreadsheet miracle around month 31. The stronger model is less glamorous. It shows cohorts, hires, tooling, conversion, churn, gross margin, payback, and the assumptions a partner will actually poke. It does not need to be fancy. It needs to survive questions.

AI can help build the model faster, but it cannot decide what you understand. The founder still has to know why each driver moves, what breaks first, and which assumption is doing too much emotional labour. If your model cannot explain the business, the problem is not Excel. It is the business being slightly too vibes-based for the room you are entering.

Doggy Bag

Tokenized Treasuries crossed roughly $15 billion. This is the part of crypto that sounds least exciting and may therefore become the most institutional: regulated-ish yield, 24/7 transferability, collateral usage, and a nice boring Treasury wrapper. The future of finance occasionally looks like a money-market fund that learned to move after dark.

Picking up the phone is becoming premium behavior. As inboxes fill with AI-assisted outreach, a real call with a real human may start to feel oddly luxurious, like handwritten notes or hotels that still answer reception. Automation is useful. But if everyone automates the first touch, the scarce asset becomes a human who can actually listen without trying to scale themselves mid-sentence.

Launch communities are turning attention into a semi-productized channel. Founder groups, maker networks, upvote brigades, directory launches: all of it says the same thing. Distribution is now something founders try to rent, borrow, and batch-process. Helpful, yes. But it still cannot rescue a product whose only clear user is “people on the internet, ideally many.”

Founder success has a strange emotional accounting problem. The second the money works, purpose, boredom, ambition, guilt, and identity all walk into the same room and refuse to sit quietly. The market loves exit stories because they are clean. The human after the exit is usually less clean, which is probably why it is more interesting.

What to watch

Watch the U.S. crypto market-structure debate. Stablecoin rewards, developer protections, and token classification will shape which rails get to become boring enough for institutions.

Watch Circle’s Arc and Agent Stack adoption. The question is not whether the announcement sounds futuristic; it is whether developers and institutions actually route activity through it.

Watch credit volumes if rates start easing. Lending AI will look much more exciting once originations stop behaving like a sad elevator.

Watch AI infrastructure outside GPUs. Power, cooling, networking, and operational reliability are where a lot of the margin conversation may move next.

Watch founder models. In a market that still funds ambition, the fastest way to lose credibility is to show numbers that cannot explain themselves.