SuperCharger Malta showed what a serious accelerator can do when its partner network is real. It also reminded me of a recurring lesson from venture investing in EdTech and Future of Work: solving a global problem, delivering a polished demo-day pitch, and benefiting from a strong ecosystem are not, on their own, enough to create venture-scale distribution.

I went to Malta expecting the familiar demo-day format: founders on stage, investors in the room, partners around the edges, and a compressed attempt to turn months of accelerator work into a few hours of attention. That format exists because early-stage markets need compression. Nobody has time to meet every founder one by one, read every deck properly, reconstruct every market, and understand every local ecosystem from scratch. A good demo day reduces the friction of discovery by concentrating founder energy, investor attention, partner relationships, government support, and a lot of invisible preparation into one room.

The problem is that anyone who has been to enough of them knows the standard pattern. A few polished pitches. A few companies that are too early but charming. A few investors taking polite notes. Some conversations at the coffee break that feel warmer in the moment than they will look in the CRM three weeks later. Then everyone goes back to their calendar and the real question starts later, away from the stage: who actually follows up, who has a case strong enough to carry internally, and which companies were mostly benefiting from the temporary intensity of the room?

This one felt different enough to write about, not because every company on stage was immediately venture-backable, but because the event exposed something more interesting than a simple “good cohort” or “bad cohort” judgment. SuperCharger Malta showed what happens when an accelerator is not merely running a presentation program, but trying to build a market-access machine around a specific vertical. It also reinforced a recurring observation from venture investing that sits underneath a lot of EdTech and Future of Work investing: global relevance is not the same thing as venture scale.

I was invited as an investor through the Collektiv Club, Ugly Baby, and Tenity orbit, and I had no fixed expectation going in. I knew SuperCharger Ventures had a clear EdTech and Future of Work focus. I knew Malta had been making a visible push around startups and technology. I knew Malta Enterprise was involved. I also knew, from years of seeing accelerators from the inside and outside, that the words “ecosystem,” “partners,” and “access” can mean almost anything. Sometimes they mean actual commercial leverage. Sometimes they mean a slide with logos.

In Malta, the logos felt less decorative than usual. The organization was unusually tight. The founders had clearly been trained without being over-sanded into identical pitch machines. The sessions moved well, staying entertaining, despite over 40 consecutive pitches. The room had the right kind of density: investors, ecosystem operators, government-linked actors, corporate partners, and founders who understood why they were there. More importantly, SuperCharger’s collaboration with Classera, Malta Enterprise, and other partners appeared to have commercial substance. In several cases, companies were not merely being introduced to partners as a vague future possibility; they seemed to have active or emerging business relationships with the partner network around the program.

That distinction matters more than most accelerator marketing admits. The lowest-value accelerator product is curriculum plus community. The better product is selection plus network. The much better product is structured market access, where the accelerator can help a company test whether the customer, partner, regulator, distributor, or channel actually behaves the way the deck claims it will behave.

SuperCharger’s public Malta program is positioned as a 12-week, equity-free accelerator for EdTech and Future of Work companies expanding into Europe, with support from Malta Enterprise and access to a global EdTech ecosystem.

As part of this well organized event, SuperCharger announced a EUR10 million vehicle to back cohort companies, which changes the nature of the platform. An accelerator that can source, train, commercially surround, and then selectively capitalize its strongest companies is no longer just selling exposure. It is trying to become a vertical financing engine. Pair that with SuperCharger’s claim that it sees roughly 20% of worldwide EdTech dealflow, and the strategic ambition becomes clearer. I treat sourcing claims carefully, as any investor should, but even directionally, it points to something rare in the category: a potentially advantaged filter in a market where early signal is noisy, geographically scattered, and hard for generalist investors to parse.

The stronger the accelerator, however, the more interesting the harder question becomes. If the program is well run, if the partners are real, if the founders are prepared, and if the room is credible, then the problem is no longer whether the event was professional. The problem becomes more useful and more uncomfortable: what actually converts an impressive accelerator company into a fundable venture case?

That is where the day became valuable to me. Not as a beauty contest, and not as a cheerleading exercise for EdTech, but as a live demonstration of the gap between startup quality and venture shape. A company can be meaningful, useful, revenue-generating, partner-supported, and still not yet be a venture-scale case. That sentence sounds harsh only if we confuse venture capital with general business validation. They are not the same thing. Venture capital is a particular financing product with a particular return requirement, and its appetite is considerably narrower than many founders first assume.

Jurisdiction is Part of the Product

Malta itself is part of that story. The island is doing visible work to attract startups, and you can feel the effort in the way the ecosystem presents itself: government support, startup events, a technology narrative, and a desire to position Malta as a bridge between Europe, MENA, and international markets. The historical scenery is almost absurdly beautiful, which does not hurt, but the more important investor question is not whether Malta is charming. It is whether Malta can become operationally useful.

This is where I found myself wanting Malta to speak with a sharper administrative confidence. Estonia has built a very clear story around company formation as a product: incorporation, digital operations, remote founder comfort, and the general sense that a company can exist there without drowning in procedural fog. Founders understand that story quickly. Investors understand it too, because clean administration reduces friction, and friction matters more at the early stage than people think. If a startup is going to build from a smaller country, that country has to make the company easier to create, easier to govern, easier to finance, and easier to explain.

Malta already has many of the ingredients. It can talk about its beauty, English-speaking environment, strategic location, access to Europe and MENA, and the warmth of its startup ecosystem. Those are genuine advantages, but they are increasingly table stakes for founders choosing where to build.

Where I think Malta has an even bigger opportunity is to tell a stronger administrative story. Easy company formation, investor-friendly regulation, practical founder support, clear incentives, and the feeling that a company can land, start operating quickly, and reduce complexity rather than add it. That may sound like bureaucracy, but from a venture perspective it is infrastructure. Early-stage companies do not need more romance from a jurisdiction. They need leverage.

For founders, the choice of incorporation and operating base becomes part of the financing narrative whether they like it or not. Investors may not say this politely in the first meeting, but they are always asking whether the company is going to be easy to finance, diligence, govern, and eventually acquire. Jurisdiction, incentives, administration, partner access, and investor familiarity all feed into that. Malta seems to understand pieces of this. My constructive criticism is that it should make the whole thing more explicit. If the country wants to be a serious early-stage landing zone, it should brag less like a destination and more like infrastructure.

Global Problems, Local Markets

The cohort reinforced a separate but related observation I keep coming back to in venture: global applicability alone does not necessarily translate into venture scale. This matters especially in EdTech because education problems travel so easily in language, and much less easily in business model. Children need better maths tools. Teachers need better workflows. Schools need more trustworthy assessment. Workers need upskilling. Employers need training that actually changes performance. Healthcare teams need competency systems. Parents need better ways to understand learning and development. These problems exist almost everywhere, which makes them emotionally and intellectually compelling.

But a problem existing everywhere does not mean a company can sell everywhere, win everywhere, or compound everywhere. That is the trap. A founder says “this is a global problem,” and investors hear something different: how many different procurement systems, languages, curriculum standards, data rules, buyer incentives, budgets, cultural assumptions, school calendars, implementation requirements, and trust networks are hidden inside the word “global”? In EdTech, a global problem can actually be a warning sign if the company has not found a distribution mechanism that compresses that complexity.

The venture case begins when the company can answer a narrower question: what do you get to own if this works? Do you own a workflow that becomes harder to replace with usage? Do you own a data layer that improves the product or the commercial position? Do you own a procurement channel that gets cheaper over time? Do you own a community, a curriculum standard, a compliance position, a partner network, an assessment format, or an operating system that can become stronger with scale? Or do you own a useful product that has to be resold, re-localized, retrained, and re-justified in every new market?

That is the uncomfortable lesson from many demo days. A company can have a real mission, a credible founder, an attractive pitch, good early revenue, and meaningful partner interest, while still being incomplete as a venture case. The missing piece is often not product quality. It is the shape of distribution and the quality of revenue. Investors are not merely asking whether customers like the thing. They are asking whether the company can become more efficient, more defensible, and more valuable as it grows. In venture, growth that remains artisanal is not the same as scale.

SuperCharger’s Cohort

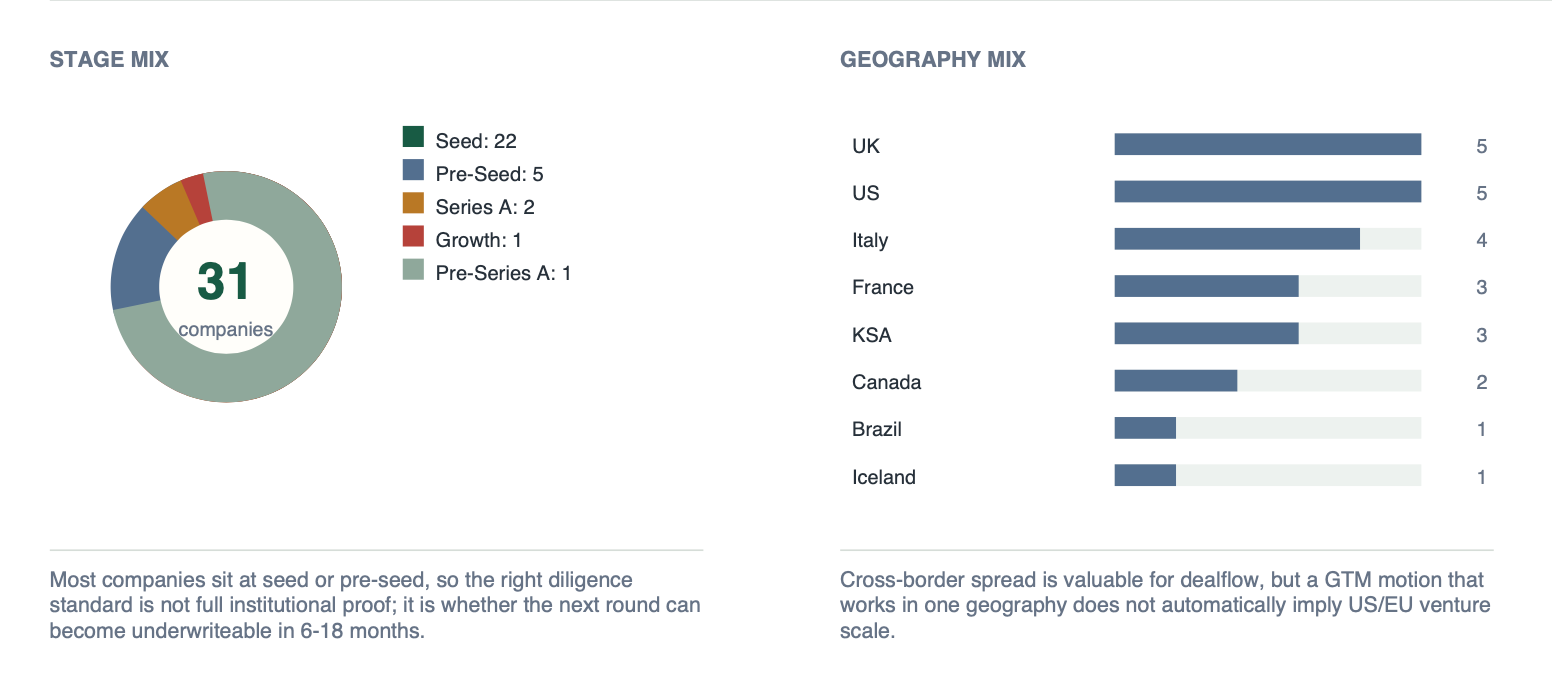

I reviewed 31 companies in the final analytical set. The stage mix was mostly early: 22 Seed companies, five Pre-Seed companies, two Series A companies, one Pre-Series A company, and one Growth-stage company. The cohort spanned 17 geographies and had 276 full-time employees across the reviewed companies. The thematic mix was clear: 21 companies touched EdTech, 11 touched AI and machine learning, nine touched Future of Work, and several sat at the intersection of health, workforce, child safety, infrastructure, fintech, music, esports, and enterprise productivity. The stated round amounts totaled roughly 44.5 million across mixed currencies, which is directionally useful but should not be treated as a clean normalized fundraising number.

That is a serious amount of company formation for one cohort, and it roughly matches where the EdTech market seems to be moving. HolonIQ’s 2026 EdTech work describes a market maturing around workforce development, institutional infrastructure, K-12 support, and AI-enabled tools embedded into existing education and career structures. That description matched what I saw in the room. This was not a parade of cute learning apps pretending that engagement alone is a business model. Many companies were attacking real workflows: assessment, teacher development, school data, regulated workforce training, mental health, health records, financial literacy, enterprise productivity, and distribution infrastructure.

The strongest VC-shaped cases were not necessarily the ones with the most moving mission or the most elegant stage performance. They were the ones where the mission connected to a repeatable buyer, a recognizable budget, some evidence of retention or recurring need, and a plausible reason distribution could become easier over time.

That is a subtle but important distinction. Impact tells you why the company should exist. Venture shape tells you whether the company can become large enough, defensible enough, and economically efficient enough to justify the financing path it is asking for.

The (almost) complete list of companies we saw:

This is not investment advice, and it is not a final ranking. It is a public version of how I would start reading the cohort as an investor. The question is not “which companies are good?” That question is too vague. The better question is: which companies already have the beginnings of a case that can travel from a demo day into an investment committee conversation without collapsing under basic diligence?

Pandatron stood out as one of the clearest VC-shaped cases in the cohort because the company seemed to sit closer to enterprise execution infrastructure than to generic coaching software. It is building an AI management consultant, and based on the materials reviewed, it had stronger signals around ARR, enterprise logos, repeat customers, weekly usage, and consultant-referral distribution. That does not make the case automatically easy. The diligence burden is significant: ARR quality, logo concentration, security posture, deployment motion, expansion behavior, and whether usage survives beyond an initial champion all matter. But the venture-grade version of the company is legible. If Pandatron becomes a system through which organizations operationalize management routines, follow-through, change programs, and team execution, then it is not selling “AI advice.” It is selling managerial infrastructure.

The Learnery read as institutionally serious for almost the opposite reason: regulated workforce training is not a sexy phrase, which is often why it can be commercially interesting. The company sits around healthcare and competency development, a category where training is not merely a feel-good HR benefit. It can be tied to compliance, role readiness, institutional risk, and measurable operational requirements. The venture case depends on whether The Learnery can move from useful training product into recurring enterprise infrastructure: repeatable deployment, renewals, expansion within accounts, and partner-sourced pipeline in a focused regulated segment. The more it can prove that training is not a one-off content sale but part of an ongoing workforce operating system, the more investable the story becomes.

University Startups had an attractive shape because it is tied to a mandated education workflow. That matters. Compliance-driven pain behaves differently from aspirational learning improvement. When a school district has a legal, administrative, or accountability reason to care, urgency and budget can become less sentimental and more concrete. The questions are still serious: ARR, ACV, retention, procurement cycles, implementation load, and the ceiling of the category. But the wedge is more venture-legible than generic student support because the buyer’s pain is not just “we would like better outcomes.” It is closer to “we have a required process that is currently painful, risky, or inefficient.”

Tokidos was one of the more commercially legible consumer cases, and consumer is where I become especially careful. Hardware can make a young company look more mature than it is because units sold, product photos, retail conversations, and parent enthusiasm create visible momentum. But hardware can also punish founders through inventory, margin, tariffs, channel costs, seasonality, returns, and working-capital demands. What made Tokidos interesting was the presence of real revenue and product behavior evidence. The venture case, however, depends on what sits behind the device. If the installed base becomes a recurring, high-margin content, games, IP, and

subscription platform, the company starts to look like a scalable child-learning ecosystem. If it remains primarily hardware with periodic content, the business may still be good, but the venture math becomes harder.

Finanz was interesting because the better reading is not “financial education app.” Financial education alone is a difficult venture category. Users may like it, regulators may appreciate it, and partners may endorse it, but the willingness to pay can be weak and the engagement curve can fade after the first burst of motivation. The more compelling version of Finanz is as a trusted intent, data, and conversion layer for financial services, especially for first-time investors or younger consumers entering regulated financial products. That is a much bigger and more delicate business. It requires activation, consented data, regulated conversion, trust, and revenue quality. If those elements work, the company is not simply teaching people about finance. It is sitting near the point where financial intention turns into financial action.

Daigon was one of the more coherent category wedges in the cohort: international and independent school esports, with association-led distribution and early revenue. I like category wedges when they are narrow enough to win and strange enough that incumbents are not paying full attention yet. School esports has that quality, especially where identity, competition, student engagement, and institutional programming intersect. The risk is also obvious. The niche has to become large enough before bigger scholastic esports platforms, federations, publishers, or school networks absorb the opportunity. Still, the shape was clear, and clarity is underrated. Investors do not need every early company to have all the answers. They need to see what the company is trying to own.

SIYA had a real classroom wedge around handwritten exams and assessment insight. In a world where written assignments are increasingly polluted by AI assistance, the idea that paper becomes smarter is more interesting than it first appears. The company’s potential is not simply in digitizing handwriting; it is in turning analog assessment moments into structured insight for teachers, schools, and possibly institutions that need higher-trust evidence of learning. The diligence questions are exactly where they should be: signed ARR, procurement conversion, EU compliance, IP ownership, margin profile, and whether Malta or EU pilots can repeat outside the initial partner context. The opportunity is timely, but the company has to prove the workflow becomes embedded rather than episodic.

Coraltalk sits near a similar assessment shift. Written assignments are losing some of their signaling value, not because writing is dead, but because educators increasingly need to know whether a student can explain, defend, and reason through what was submitted. Oral assessment, active recall, and spoken explanation may become more important as AI-generated text becomes ordinary. The investor question is whether Coraltalk can own a durable assessment workflow or whether it becomes a feature inside LMS, AI tutor, classroom management, or assessment platforms. This is the kind of company where timing can be excellent and defensibility still has to be earned.

Ayamedica looked like a credible regional vertical SaaS candidate around school and clinic health records, especially if partner access in MENA converts into retained, paid, low-friction institutional revenue. Health records in education-adjacent settings are not glamorous, but they can sit inside mandatory workflows where reliability, trust, and continuity matter. Spyro Global attacked a different but important EdTech bottleneck: international distribution. Helping suppliers manage partners, showcase products, and track sales is valuable if the platform captures recurring or transactional economics rather than simply brokering introductions that later move off-platform. Humanava had an interesting simulation and behavioral-assessment angle, especially if it can escape bespoke leadership-training delivery and become scalable infrastructure for how organizations evaluate and develop management behavior.

A strong cohort should not be reduced to the handful of companies that are easiest to discuss through an institutional VC lens. One of the useful things about SuperCharger Malta was precisely the range of company formation it brought into the room, because that range showed how broad the EdTech and Future of Work umbrella has become.

Anathem is applying AI to paperwork-heavy frontline workflows in healthcare and policing.

AtlasVR is building AI-powered XR training for industrial procedures.

Discentis is working on teacher professional development and community, a category where trust and adoption matter as much as content quality.

Synegram is an original MusicTech and EdTech IP case around visual music understanding.

Elevify is building an AI learning engine with international reach.

Expando AI focuses on partner enablement for sales and partnership teams.

Fahman is building Arabic and English children’s audio and digital books for family audiences in the Arab world.

Several companies were closer to operational tooling than traditional education content.

Frizzle is working on handwritten math grading and teacher workflow.

GetBOB is building a marketplace for custom AI employees.

KidzRise focuses on early talent detection for children. meritt applies AI to sales talent discovery, development, and matching.

Jusoor Labs builds immersive 3D simulations and virtual labs.

Lynx Educate connects corporate education investment with social mobility.

Myndoor combines psychologists, coaching, and AI-driven employee wellbeing.

Peerbie is building an AI-powered work OS with an execution layer.

Prodevs combines global tech talent access with AI hiring tools.

Salute360 is building a digital health platform for patients and healthcare providers.

Sylenze is working on safe media storage and distribution infrastructure for schools.

EverybodyCounts is focused on affordable primary maths mastery with social impact.

Evolytes is changing how children learn maths through an Icelandic EdTech platform.

That range is a strength for an accelerator and a challenge for investors. If you look only at demo-day polish, many of these companies sound strong. If you look only at social value, many are easy to admire. If you look only at global applicability, almost all can tell a large story. But institutional venture is less forgiving because it has to translate admiration into ownership, ownership into fund returns, and fund returns into a credible underwriting case before the investor has perfect information.

The real questions are narrower and more demanding. Who pays? How often? How much? How long does the sale take? Does retention prove the product is embedded, or merely liked? Is the revenue truly recurring ARR, or a mixture of pilots, training, implementation, grants, services, and partner-funded experiments? Does distribution compound, or does every new market require fresh trust-building from zero? Does the company own a workflow, a data layer, a compliance layer, a community, a procurement channel, or a category position that becomes stronger with scale? If the company wins, does the outcome become large enough to matter to a fund after dilution?

This is where SuperCharger’s opportunity becomes especially interesting. The organization already seems good at community, pitch preparation, partner access, and thematic sourcing. That is not trivial. Many accelerators never get that far. The next frontier is a more explicit venture-conversion layer: helping founders understand not only how to pitch, but how their company will be read by institutional capital after the applause is gone.

That layer would make the program more valuable precisely because it would introduce uncomfortable questions earlier. Is this partnership a distribution moat, or only access? Is this traction repeatable without the accelerator’s halo? Is this a venture-scale company, or a strong education business that should consider a different capital path? What milestone would actually change the financing answer, rather than simply make the company look busier? What would need to be true for a serious investor to argue the case internally without relying on goodwill toward the sector?

Those questions are not negative. They are respectful. They give founders a better chance of raising the right capital from the right people at the right time, and they protect accelerators from the common trap of optimizing for stage performance rather than financing readiness.

The kindest thing an ecosystem can do for a founder is not always to make them sound more impressive. Sometimes it is to help them understand exactly where the investment case breaks before they spend their best intros discovering it in silence.

That is probably the highest compliment I can give SuperCharger after Malta: the program already has enough substance that the harder questions are worth asking. A weaker accelerator can hide behind stagecraft. A mature accelerator is able to engage with the reality that, not every strong company is ready for institutional venture, and then build the operating system that helps more of them get there.

My experience in Malta made me more interested in SuperCharger, not less. It also made me more convinced that EdTech and Future of Work investing needs a sharper vocabulary. We need fewer generic debates about whether education matters. Of course it matters. We need better debates about distribution, budget ownership, workflow control, evidence quality, recurring revenue, administrative infrastructure, and whether the company can become more powerful as it grows.

Having attended and organized many accelerator demo days over the past decade, I came away with a lot of respect for SuperCharger. The criticism in this article reflects a higher standard rather than disappointment. The accelerator has already solved many of the problems others are still struggling with. Precisely because of that, the next challenge is no longer producing polished demo days, but helping more companies cross the final gap from promising startups to institutionally investable venture cases.

That is the line between a good demo-day company and a fundable venture case. In Malta, that line was visible in a useful way: not as a criticism of the cohort, but as the work ahead for any ecosystem ambitious enough to convert global educational need into companies that institutional capital can actually underwrite.