Morning. The AI market has reached the elegant stage where everyone still says “innovation,” but the paperwork increasingly says power contract, data center lease, and depreciation schedule. Very romantic. Nothing says frontier technology like a 500-megawatt facility, a lender presentation, and someone asking whether the transformer delivery date is real.

Today is mostly about compute becoming less like a product feature and more like real estate with a model attached. If AI is the new electricity, the useful question is not who has the prettiest lamp. It is who has secured the grid connection.

Menu Of the Day

Markets: AI still carries the tape

The article: compute asks for a lease

Shot: voice fraud, PMs in the repo, and finance gates

Startup Lesson: capacity before magic

Doggy Bag: megawatts after breakfast

What to watch: the next bottleneck

Market pulse

Quick note: market data below reflects the latest available session before drafting, after the long U.S. holiday weekend and last week’s Nvidia results.

Markets: The AI trade still has the market’s attention. Nvidia’s latest quarter gave investors another reason to believe demand is not quietly fading: $81.6 billion in quarterly revenue, a stronger-than-expected forecast, and a new reporting structure that separates hyperscale from AI cloud, industrial, and enterprise demand. That split matters because the market is trying to answer a less glamorous question now: how much of AI is one giant chip cycle, and how much is becoming durable infrastructure?

Movers: The answer is showing up around the stack. Blackstone and Google are turning TPUs into a compute-as-a-service company. Nebius is talking about gigawatts and AI factories, not just cloud dashboards. Voice-security startups are raising small rounds because the fraud surface is widening while cloud providers quietly exit old authentication products. Translation for founders: capital is still available, but it is moving toward bottlenecks you can measure.

The article

AI - Infrastructure - Compute asks for a lease

The AI story used to be easy to narrate. A model got better, a demo went viral, a founder added “agent” to the deck, and everyone pretended the future had politely arrived in a browser tab.

That version is not dead. It is just no longer the whole story.

The new AI story has a landlord. Blackstone and Google announced a joint venture to create a TPU cloud, with Blackstone making an initial $5 billion equity commitment and the company expecting to bring 500 megawatts of capacity online in 2027. Google brings the chips and technical stack. Blackstone brings infrastructure capital, data center muscle, and the patient ability to make something very expensive look normal in a spreadsheet.

Quick reminder: 500 megawatts is not a feature launch. It is an industrial asset. It needs land, power, cooling, networking, permitting, equipment, financing, and customers willing to sign enough demand to make the whole thing less terrifying. AI is still software at the user interface. Underneath, it is increasingly a project-finance animal wearing a hoodie.

Nebius tells the same story from a different angle. The company reported first-quarter results this month and said it had secured up to 1.2 gigawatts of power and land for a new owned AI factory in Pennsylvania. The useful word is not “factory” because it sounds futuristic. The useful word is “secured.” In a constrained market, access to power, sites, chips, and delivery timelines becomes strategy, not operations.

In practice: this changes what founders should pay attention to. If you are building an AI application, your margin story depends on someone else’s infrastructure decisions. If you are building AI infrastructure, your pitch is not only model demand. It is utilization, power access, customer concentration, financing cost, hardware supply, and whether your capacity will still be valuable when the next chip generation arrives.

The catch: capacity cuts both ways. When demand is scarce, software companies fight for attention. When capacity is scarce, buyers fight for slots. But if everyone finances the same capacity at the same time, the bottleneck can move. It may shift from GPUs to power, from power to interconnects, from interconnects to enterprise workloads that actually justify the bill. The bottleneck is mobile. Very annoying. Also where the money tends to hide.

This is why Nvidia’s reporting change matters beyond the stock ticker. Separating hyperscale from AI cloud, industrial, and enterprise demand is a way of telling investors: do not think of this only as chips sold to a few giants. Think of it as infrastructure demand spreading into more end markets. Whether the market fully buys that framing is the next test.

For investors, the lesson is uncomfortable but useful. AI winners may look less like pure software miracles and more like hybrids: part semiconductor supply chain, part cloud platform, part energy customer, part financing vehicle. The returns can still be enormous. The failure modes just become heavier. A bad SaaS quarter gives you churn. A bad infrastructure bet gives you stranded assets, debt service, and a data center full of expensive optimism.

For founders, the practical read is simpler. The cheapest AI strategy is not always the smartest one. The fastest model is not always the most defensible one. And the prettiest product demo matters less if the unit economics assume infinite cheap inference from someone else’s balance sheet.

Zoom out: AI is becoming more real, not less. Real things have invoices, bottlenecks, depreciation, counterparties, and contracts. That is good news for serious builders. It means the market is maturing past vibes. It also means the next edge may belong to the teams that understand the physical and financial plumbing under the magic trick.

Shot

Voice authentication gets awkward

London-based Voxmind raised a small pre-seed round for on-device voice biometrics and deepfake detection, and the timing is the interesting part. Microsoft retired Azure Speaker Recognition in 2025, and AWS Voice ID support ends this month. When cloud giants step away from a security surface just as AI voice fraud gets better, niche startups get a wedge. Not every big opportunity starts with a giant round. Some start with an abandoned control point.

PMs move closer to the repo

A fresh product newsletter framed Codex as a way for PMs to work inside a repo without living in the IDE: file tree, diffs, skills, MCPs, and a second reviewer next to Claude. The bigger signal is not which coding assistant wins a workflow screenshot. It is that product work is moving closer to executable systems. The PM who can inspect the product surface, the prompt layer, and the code path will have a different kind of leverage.

Finance agents find the gates

The useful part of the agentic-close conversation is not that a finance agent can pull data and draft journal entries. It is that the workflow stops at explicit human gates: rate lock, data review, billing decisions, final approval. That is where enterprise AI becomes buyable. Autonomy without gates is a demo. Autonomy with gates starts to look like operations.

Mega-rounds keep narrowing the field

Recent venture mega-rounds in AI infrastructure and universal interfaces show that capital is still aggressive where the story is large enough. The catch is that the bar has moved from “AI is big” to “this company could own a layer.” That is a much harder sentence to prove, which is probably healthy for everyone except founders currently polishing slide 17.

Startup Lesson

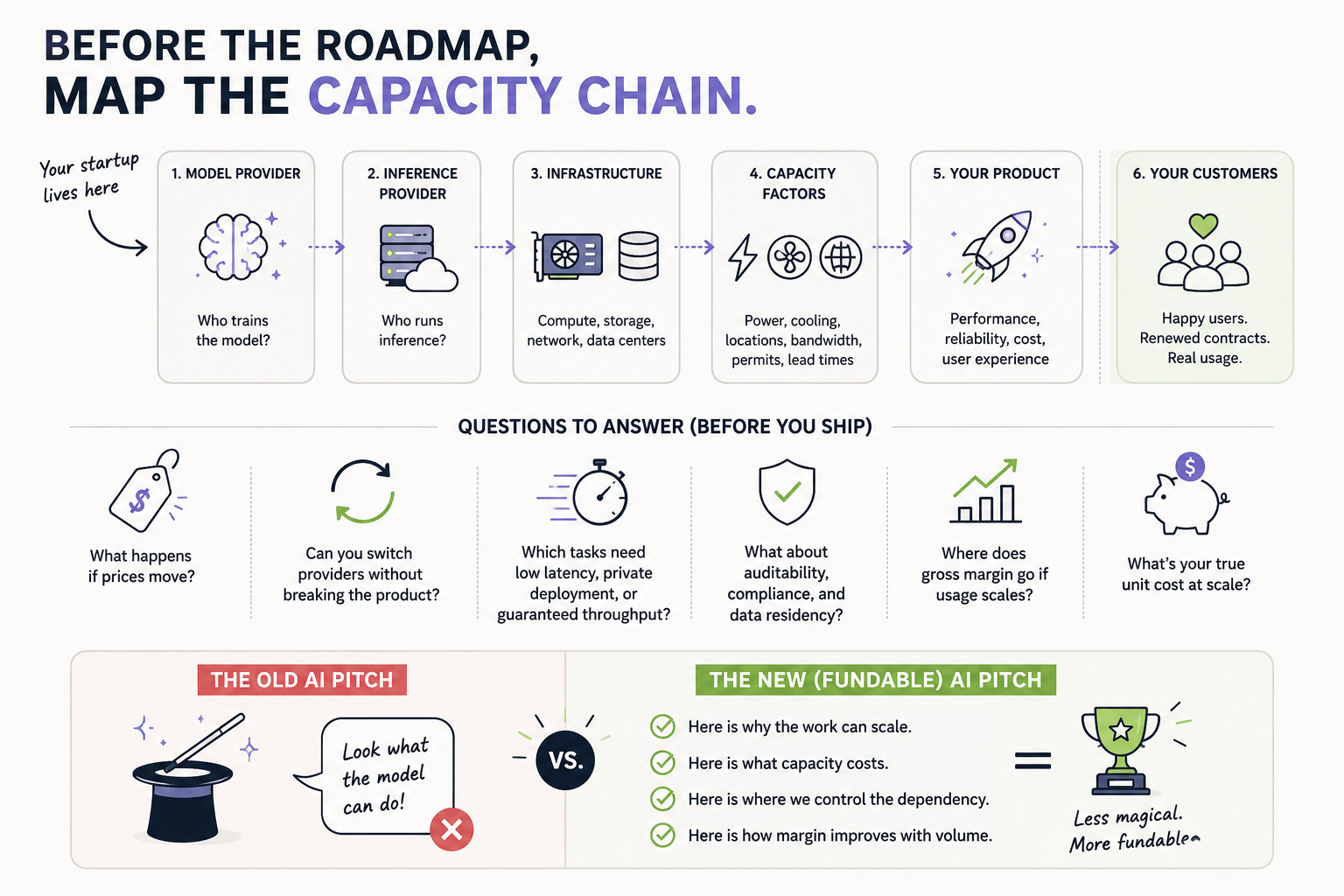

Capacity before magic

If your startup depends on AI, map the capacity chain before you map the feature roadmap.

Who provides the model? Who provides inference? What happens if prices move? Can you switch providers without breaking the product? Which tasks need low latency, private deployment, auditability, or guaranteed throughput? Where does gross margin go if customers actually use the product as much as you hope?

The best AI pitch is no longer only “look what the model can do.” It is “here is why the work can scale, here is what capacity costs, here is where we control the dependency, and here is how margin improves with volume.” Less magical, more fundable.

Doggy Bag

Fun fact: the most exciting AI phrase of the week may be “500 megawatts.” Terrible on a billboard. Excellent in an infrastructure memo.

The number: 1.2 gigawatts. That is the power-and-land capacity Nebius says it has secured for a Pennsylvania AI factory. AI cloud is becoming a land-and-energy game with software margins as the dream.

The quote: “The bottleneck is mobile.” Today it is chips, tomorrow power, next quarter enterprise adoption, and eventually someone in procurement who just wants the invoice to make sense.

Reco: before falling in love with an AI product, ask what happens at 10x usage. If the answer is “we will call our cloud provider and hope,” keep asking.

And besides that

- Nvidia’s new reporting structure is worth watching because market categories shape investor patience.

- Enterprise AI services are starting to look like implementation companies with model-provider logos attached.

- On-device security is getting more interesting as synthetic media moves from funny clips to bank-call risk.

- European startups with narrow compliance or security wedges may benefit from big-platform exits, not only from big-platform APIs.

- The AI PM tooling conversation is quietly becoming a labor-market conversation: who gets to touch the production system?

What to watch

Watch whether TPU alternatives become real procurement options for enterprises, or mostly another hyperscaler-adjacent capacity channel.

Watch power and site announcements from AI clouds; the next bragging right may be secured megawatts, not only benchmark scores.

Watch Nvidia’s AI cloud, industrial, and enterprise reporting line for evidence that demand is broadening beyond hyperscalers.

Watch voice fraud and deepfake authentication because abandoned cloud products can become startup markets quickly.